We get it—debt is a four-letter word no one likes to talk about.

But here at Credit Connection, we don’t just talk; we empower our clients with the knowledge and tools they need to take control of their financial future.

This debt consolidation guide will show you the ropes, from understanding what debt consolidation is, to whether it’s the right choice for you, and how you can go about it.

What You'll Gain from This Guide

• A clear understanding of what debt consolidation entails • Insight into whether debt consolidation is the right path for you • Alternatives to debt consolidation • An overview of how Credit Connection can be your ally in this journey

Before you consider taking out a debt consolidation loan, it’s crucial to examine your circumstances carefully.

Consolidation could be either a solution or a pitfall, and this guide will help you determine which.

Understanding Debt Consolidation and its Benefits

Think of debt consolidation as your financial Swiss Army knife. It folds all those high-interest debts—credit cards, personal loans, you name it—into one manageable payment at a lower interest rate.

This simplifies your monthly payments and can potentially save you a substantial amount of money. Plus, by reducing your overall interest rate, you’re able to pay off the principal balance faster, accelerating your path to debt-free living.

What is Debt Consolidation?

Debt consolidation could involve taking out a new loan to pay off existing debts or transferring outstanding balances to a single credit card with a lower interest rate.

Common Types of Debt Consolidation

1. Personal Consolidation Loans: An unsecured loan that pays off your multiple debts. You then make one monthly payment to the new lender.

2. Home Equity Loans or HELOC: Secured loans that tap into the equity of your home to pay off debt.

3. Balance Transfer Credit Cards: Credit cards with low or 0% introductory rates where you can transfer your existing credit card balances.

4. Debt Management Plans: A third-party agency negotiates with your creditors to consolidate debts into one monthly payment.

Is Debt Consolidation Right for You?

Debt is a part of life for most people, but it becomes problematic when it begins to interfere with long-term financial goals or daily living.

Debt consolidation isn’t a one-size-fits-all solution. Its effectiveness largely depends on your financial habits, the amount of debt you have, and the terms of your current loans. Here are some factors that can help you determine if this path is right for you:

1. High Interest Rates: If you have loans or credit cards with high interest rates, consolidation can save you money.

2. Multiple Monthly Payments: Juggling multiple payments can lead to mistakes and late fees. Consolidation simplifies this process.

3. Financial Discipline: If you have the discipline not to accrue more debt while paying off the consolidation loan, you’re a good candidate.

Benefits of Debt Consolidation

Simplified Life: One loan, one interest rate, one monthly payment. No more forgetting due dates.

Save Money: A lower interest rate means more money in your pocket.

Boost Your Credit Score: On-time payments with your new loan can improve your credit score.

Disadvantages of Debt Consolidation

Risk of Higher Costs: Some debt consolidation options, especially those secured against assets like your home, may have lower interest rates but longer repayment terms, which can result in higher overall costs.

Fees and Penalties: Consolidation loans may come with origination fees, and balance transfer cards may charge transfer fees. Also, there could be penalties for paying off your original loans early.

Psychological Trap: The immediate relief of consolidating your debt can sometimes lead to complacency, causing some people to accrue new debts before the consolidated debt is paid off.

How Credit Connection Can Help

At Credit Connection, we’re not just a service; we’re your financial ally. Our comprehensive debt solutions, expert advice, and robust support system are tailored to your unique financial needs.

Ready to get started?

Credit Connection's Top Debt Consolidation Tips

Know What You Owe

💡Tip: Before you can think about consolidating, you need to know exactly what you owe. Compile a list of all your debts, the corresponding interest rates, and monthly payments.

🎯Action Step: Use Credit Connection’s Debt Assessment Tool to get a clear picture of your debts and potential savings from consolidation.

Check Your Credit Score

💡Tip: Your credit score is pivotal for loan approval and interest rates.

🎯Action Step: Use our Credit Score Checker to find out where you stand and what you can do to improve your score.

Understand Eligibility Criteria

💡Tip: Lenders look at more than just your credit score. Your debt-to-income ratio and income stability are also crucial.

🎯Action Step: Consult with us to assess your eligibility for different types of consolidation loans.

Explore Your Loan Options

💡Tip: Not all debt consolidation loans are created equal. Different types have different benefits and drawbacks.

🎯Action Step: Book a consultation with us to identify the loan type that best fits your situation.

Prepare Your Application Like a Pro

💡Tip: A well-prepared application can speed up the approval process and potentially get you a better interest rate.

🎯Action Step: Use an Application Checklist to gather all the necessary documents beforehand.

Don’t Overlook the Fine Print

💡Tip: Pay attention to fees, terms, and conditions of your new loan.

🎯Action Step: Let our experts review the terms to ensure you’re getting a fair deal.

Verify Old Debts are Paid Off

💡Tip: Don’t assume that your old debts are automatically paid off after consolidation.

🎯Action Step: We can coordinate with your new lender to make sure all old debts are settled.

Re-Establish Your Budget

💡Tip: Your new loan will have different payment terms, and possibly even a different due date.

🎯Action Step: Let us help you integrate this new payment into your budget seamlessly.

Cultivate Financial Discipline

💡Tip: Consolidation is a fresh start, not a cure-all. Maintain financial discipline to avoid falling back into debt.

🎯Action Step: Use our suite of budgeting tools to keep your spending in check.

Keep an Eye on Your Financial Health

💡Tip: Regularly review your financial situation to adapt to any changes and make sure you’re on track.

🎯Action Step: Schedule quarterly financial reviews with us to adjust your financial plans as needed.

What's Your Next Move?

Top 5 Takeaways:

1. Don’t Go Solo: The intricacies of debt consolidation require professional guidance. We’re here for you.

2. Eligibility is Key: Know your credit score and debt-to-income ratio before diving in.

3. Choose Wisely: Not all consolidation loans are created equal; make sure you pick the one that benefits you the most.

4. Application Acumen: A well-prepared application can be your ticket to a lower interest rate.

5. Financial Discipline: Post-consolidation, discipline is your best friend to ensure you don’t fall back into debt.

Consolidating your debts is a significant step towards financial freedom, but maintaining that freedom requires ongoing effort.

Now is the time to cultivate healthy financial habits – budgeting, saving, mindful spending. We’re here to provide advice and tools to help you stay on track, from budgeting apps to savings strategies.

At Credit Connection, we’re your financial ally, providing expert advice and support every step of the way.

Ready to start your debt consolidation journey?

Schedule a conversation at a time that suits you.

Let’s work together towards your brighter financial future.

Navigating the Fixed Rate Mortgage Cliff: A Credit Connection Guide

With 12 interest rate hikes since last May and the cost-of-living ballooning, Australian households are grappling with a challenging financial landscape.

On top of this, a vast number of borrowers are about to see their fixed-rate loans expire, leading to a sudden and significant increase in their monthly repayments.

Why Fixed-Rate Mortgages Are Under the Lens

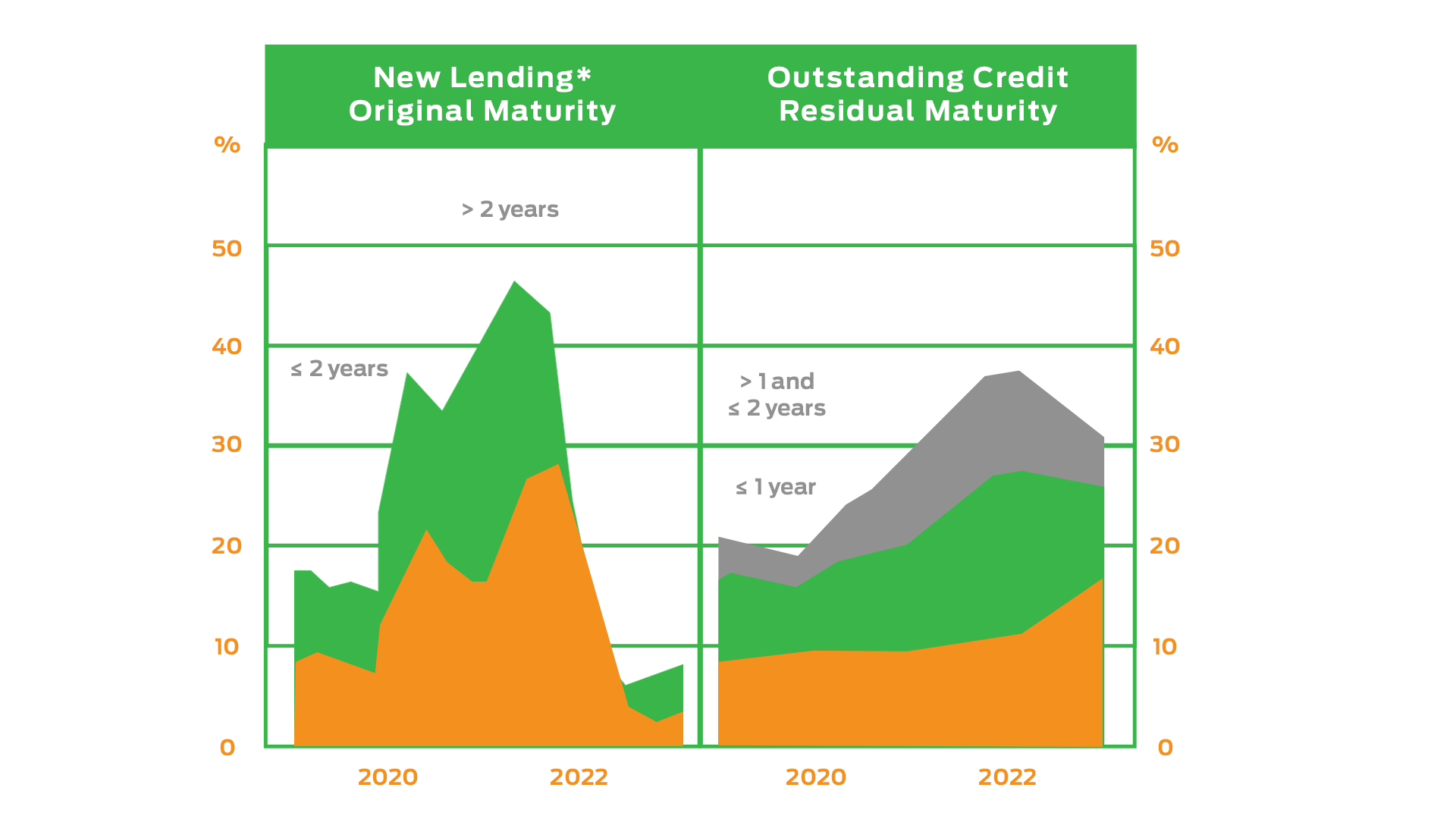

RBA data shows that the value of fixed-rate loans increased substantially during COVID-19, peaking at 40% of outstanding housing credit in early 2022.

That’s roughly twice their usual share from prior to 2020.

Sources: APRA, RBA

Some of these fixed-rate loans that expired in 2022 saw an increase of up to 50% in repayments! This trend will continue, and by the end of 2023, approximately 880,000 fixed-rate loans will expire.

With these pandemic-era fixed-rate home loans nearing their expiration dates, borrowers are at a crossroads.

Stay with their existing lenders at higher variable rates, or embark on the complex journey of refinancing, or look for a new lender altogether?

At Credit Connection, we have the expertise and data to guide you through this delicate time. In this article, we’ll explore strategies, potential pitfalls, and solutions for borrowers who are nearing the end of their fixed-rate terms.

The Cost of Complacency

If you think doing nothing is an option, think again.

When your fixed-rate term ends, your bank will likely tell you that you don’t have to do a thing. They’ll handle it all and shift you onto their standard variable rate. This transition will be presented as a hassle-free, almost charitable act.

But let’s be clear: This is far from a complimentary upgrade.

In reality, this automated switch is a revenue-generating machine for the bank. While you’re lulled into a false sense of security, thinking that everything is taken care of, your bank could be pocketing tens of thousands of extra dollars from you each year in interest payments.

That money could have been your holiday fund, your early retirement, or that dream vacation you’ve always wanted.

Why do banks do this? Because they can. And because the people who just let things roll are a significant source of profit.

You might as well be signing a check to your bank for tens of thousands of dollars—year after year.

🎯 Top 3 Actionable Tips

Question the Status Quo: If your bank says you don’t have to do anything, take it as a sign that you should probably do something.

Know Your Terms: Before your fixed rate term ends, mark it on your calendar and set reminders to start shopping for new rates at least three months in advance.

Run the Numbers: Use an online mortgage calculator to find out exactly how much more you’ll be paying if you let your mortgage roll over to a standard variable rate.

How Credit Connection Makes a Difference to Your Mortgage Rates

1. Unlocking ‘New Customer’ Rates for You: Banks usually reserve their best rates for new customers. As mortgage brokers, we leverage our extensive network to get you those elusive new customer rates, even if you’ve been with your bank for years.

2. Negotiating on Your Behalf: We don’t just stop at the first offer. We’ve sent back rate requests at the expiration of fixed periods multiple times to ensure that you’re getting the absolute best deal possible.

3. Analysing Variable Rates: While fixed rates have their benefits, variable rates can offer more flexibility and potentially lower costs over the long term. We’ll help you analyse whether this option suits your financial situation better.

4. Fresh Property Valuation: Lender rates can vary based on your property’s valuation. We facilitate new valuations to possibly lower your loan-to-value ratio, which can significantly impact your interest rate.

5. Custom Mortgage Action Plan: Every borrower is unique, and so are our financial strategies. We look at your complete financial picture to come up with a tailored plan that can save you thousands of dollars.

Preparing for the Inevitable: What Happens When Your Fixed-Rate Loan Rolls Over?

As we approach the peak of the mortgage cliff, preparation is your best defence against skyrocketing costs. Credit Connection is committed to helping you through this transition, ensuring you’re not just another casualty of the mortgage cliff.

Equity and LVR: Your Secret Weapons in the Mortgage Game

These two elements often sit quietly in the background of the mortgage landscape, overshadowed by more popular terms like “fixed rates” or “variable rates.” Yet, they wield enormous power in determining how much you pay for your home loan.

Especially in a fluctuating market, understanding your equity and LVR can be your ticket to potentially saving tens of thousands of dollars.

Equity is like a silent financial partner that grows stronger and more influential over time. It’s a resource you can leverage for various purposes, from negotiating better loan terms to even securing additional financing for investments or renovations.

A lower LVR is like a VIP pass in the mortgage world. It significantly reduces the lender’s risk, making them more willing to offer you attractive loan terms, including lower interest rates. This is especially crucial in a landscape where mortgage rates are shifting, and every percentage point counts.

How Equity and LVR Connect in Your Mortgage Strategy

Equity and LVR are intricately connected. As your equity increases, your LVR naturally decreases, assuming your property value remains constant or increases. By focusing on building equity, you’re also working to lower your LVR, hitting two birds with one stone and positioning yourself for better loan terms.

Credit Connection: Making Equity and LVR Work for You

In a credit landscape that’s continually evolving, your equity and LVR are dynamic assets that you can, and should, actively manage. They can be the key to unlocking more favourable loan conditions and giving you the upper hand in negotiations with lenders.

🎯 Top 3 Actionable Tips

Consolidate High-Interest Debt: Use your equity to consolidate other high-interest debts, effectively lowering your overall interest payments.

Quarterly Equity Check: Set a reminder to review your mortgage statements and local property values every quarter. Knowing your equity will prepare you for opportunistic refinancing.

Consult a Mortgage Broker: A mortgage broker can provide you with different loan scenarios that demonstrate how changes in your LVR could affect your loan terms.

As your fixed-rate loan term comes to a close, you’re essentially steering your financial ship towards a hidden iceberg. If you’re not prepared, the impact can be devastating.

🔥 Top 5 Tips For Navigating the Fixed-Rate Rollover

1. Fixed-Expiry Calendar Alert: Mark your fixed-rate loan expiry date like you would a medical appointment—it’s that crucial. Start looking at your options at least three months in advance.

2. The Variable Rate Money Pit: Switching to a standard variable rate without proper consideration is like throwing your money into a pit. Banks may earn tens of thousands from you—don’t let them.

3. Equity and LVR Leverage: Your home’s equity and Loan-to-Value Ratio aren’t just numbers; they’re negotiation tools. Use them wisely to get better terms, whether you stay with your current lender or find a new one.

4. Watch the Economic Indicators: Pay close attention to broader economic signals like the Reserve Bank’s interest rates and unemployment rates. These will give you clues about where mortgage rates are headed and help you make an informed decision.

5. Your Lifeline is a Call Away: At Credit Connection, we’re not just mortgage brokers; we’re your financial lifeline. A quick consultation can make the difference between years of financial strain and a future of financial comfort.

When it comes to rolling over from a fixed-rate loan to a variable one, ignorance is not bliss—it’s a one-way ticket to financial strain. Your proactive steps today can save you from future hardship. At Credit Connection, we’re committed to ensuring that your financial ship not only avoids the iceberg but sails smoothly into prosperous waters.

For more insights on home loans and financial planning, check out our Blog Section.

Less Debt More Life™

You work hard for your money – imagine your peace of mind knowing your money is working hard for you. Our Mortgage Action Plan delivers guaranteed results and allows you to start living the life you deserve.